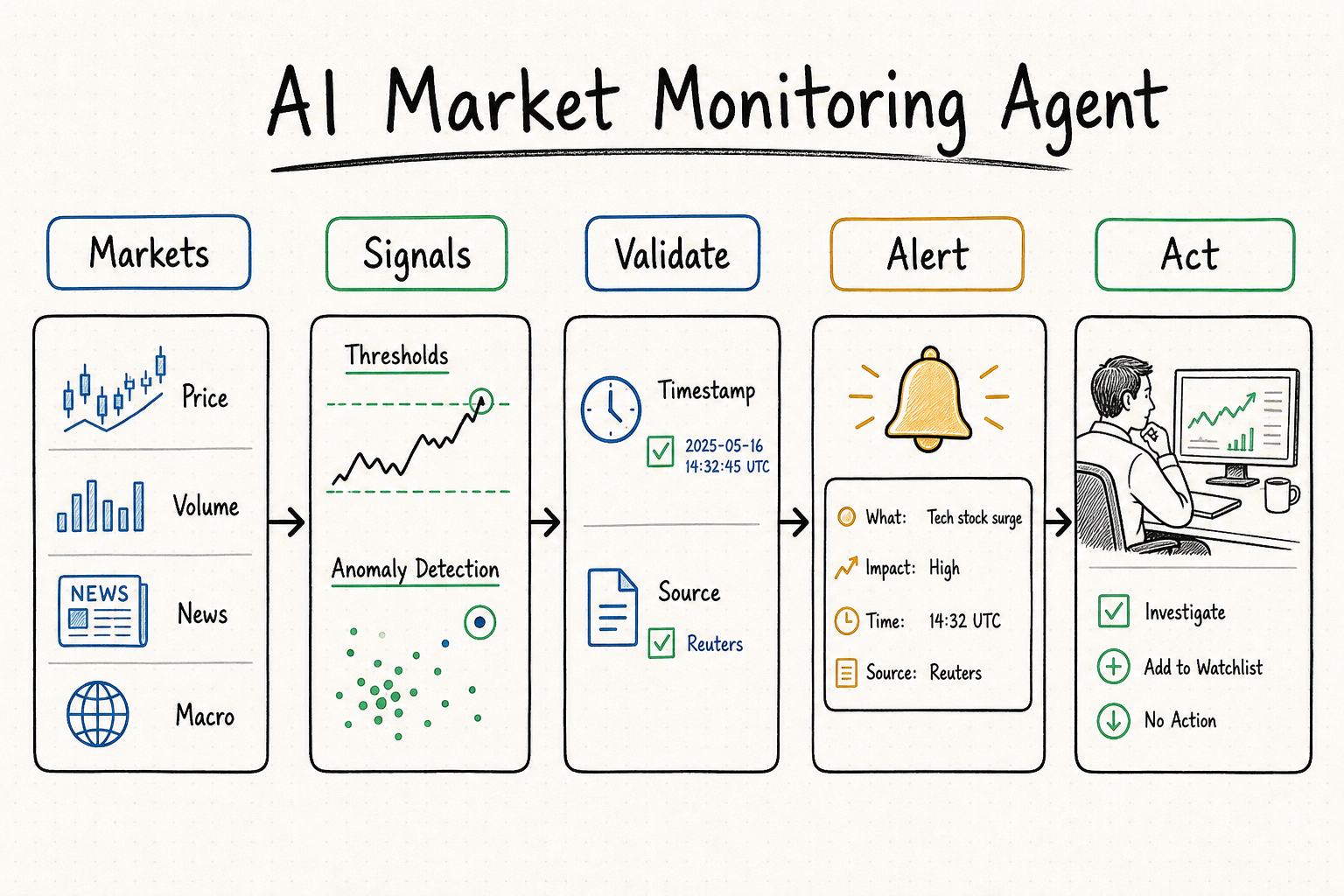

An AI market monitoring agent addresses a simple but expensive problem: financial markets generate more information than a human team can watch continuously. Quotes update in milliseconds, volume regimes change, macro releases arrive on fixed calendars, and a single headline can reprice an asset before an analyst opens a dashboard. Missing the signal is costly, but reacting to every noisy movement is equally dangerous. A well-designed agent runs 24/7, gathers relevant evidence, applies deterministic thresholds, asks an AI model to interpret context only when needed, and sends a concise alert with traceable sources. This guide shows how to build that workflow with QVeris as the capability layer and Python as the orchestration layer.

What Is an AI Market Monitoring Agent?

An AI market monitoring agent is software that automatically observes market data, identifies conditions worth investigating, and triggers a structured response. The response may be an alert, a portfolio-risk check, a research task, or a request for human review. Unlike a conventional dashboard, the agent does not depend on a person watching every panel. Unlike a single indicator script, it can combine heterogeneous evidence and explain why an event matters.

A practical market monitoring AI agent can watch real-time prices and volume, compare current behavior with historical baselines, track changes in financial news sentiment, observe scheduled releases from sources such as the Federal Reserve Economic Data service, and monitor crypto transfers or liquidity conditions. It can then produce a report containing the trigger, supporting values, source timestamps, confidence, and suggested next checks.

Developers often build rather than buy because monitoring logic is strategy-specific. A generic product may support fixed watchlists and thresholds, but a quant team may need factor-aware baselines, a fintech product may require tenant-specific permissions, and a risk team may need internal position data. Owning the orchestration also makes the alert explainable: every threshold, tool call, and model output can be logged and tested.

Key Signals for a Market Monitoring AI Agent

The quality of automated market monitoring depends less on the number of feeds than on whether each signal has a clear purpose. Start with five categories and define what constitutes a meaningful change before writing the polling loop.

Thresholds should adapt to the asset and session. A two-percent move may be extraordinary for a large-cap stock and routine for a smaller token. Use rolling distributions, median absolute deviation, or volatility-normalized returns before asking an LLM to interpret an event. Deterministic detection keeps costs predictable and reduces false positives; the model adds context after the system has established that something unusual occurred.

Why QVeris Supports Real-Time Market Monitoring AI

A monitoring system usually needs several data categories: quotes, bars, company events, news, sentiment, macro releases, and sometimes on-chain activity. Direct integrations can work, but every provider introduces a separate authentication method, schema, rate policy, retry strategy, and failure mode. QVeris provides a common capability layer across more than 10,000 financial capabilities so the application can discover and execute the tools relevant to each monitoring task.

The workflow separates three responsibilities. Discover searches for capabilities with a natural-language requirement such as “real-time US stock quote with timestamp.” Inspect returns the selected tool's parameters, output shape, provider details, latency, and cost information. Call executes the capability with validated arguments and returns structured output. This separation helps developers avoid loading every possible tool into an agent's context or hardcoding assumptions about one provider.

QVeris supports REST, a Python SDK, and MCP-based clients including Claude and Cursor. Discovery and inspection are free, while calls consume credits according to the selected capability. New accounts currently receive 1,000 credits plus 100 daily login credits; verify the latest terms on the QVeris pricing page. The architecture is most useful when an agent must combine several financial sources without maintaining a custom adapter for each one.

Step-by-Step: Build a Market Monitoring Agent

The following Python examples show a complete control flow while keeping provider-specific details flexible. QVeris capability identifiers and arguments can change as tools evolve, so always use the current QVeris documentation and the Inspect response as the source of truth. Keep API keys in environment variables and never allow model-generated arguments to bypass schema validation.

1Register and initialize the QVeris client

Create a QVeris account, generate an API key, and store it in your secret manager or local environment. Install the current Python SDK from the official docs. The reusable client below becomes the entry point for discovery, inspection, and execution.

import os

import asyncio

from qveris import QVerisClient

client = QVerisClient(

api_key=os.environ["QVERIS_API_KEY"]

)

WATCHLIST = ["AAPL", "MSFT", "NVDA", "SPY"]Separate credentials from strategy configuration. A watchlist, polling interval, and risk threshold can live in versioned application settings, while secrets remain outside source control. Production deployments should also rotate keys and redact authorization headers from logs.

2Discover real-time price and sentiment capabilities

Search by desired output rather than by provider name. One query can target a real-time quote with exchange timestamp and volume; another can target recent market sentiment with source metadata. Save the returned capability IDs so the system can inspect them before execution.

async def discover_monitoring_tools():

price_tools = await client.discover(

query=(

"real-time US stock price, percentage change, "

"volume, exchange timestamp, structured JSON"

),

limit=5,

)

sentiment_tools = await client.discover(

query=(

"recent financial news sentiment for a stock ticker "

"with article source, timestamp, and sentiment score"

),

limit=5,

)

return price_tools, sentiment_tools

price_results, sentiment_results = asyncio.run(

discover_monitoring_tools()

)Do not execute the first result automatically. Rank candidates by coverage, latency, reliability, output shape, and cost. A real-time workflow should reject delayed feeds when timeliness is a hard requirement. A research workflow may accept delayed data if the source offers better history or metadata.

3Inspect the selected tool schema

Inspection tells the application whether a tool expects a ticker, exchange, time range, interval, region, or another identifier. Convert required fields into a local validation model and refuse execution when a value is missing or unsupported.

async def inspect_tool(capability_id: str):

details = await client.inspect(

capability_ids=[capability_id]

)

return details

PRICE_CAPABILITY_ID = "CAPABILITY_ID_FROM_DISCOVERY"

price_schema = asyncio.run(

inspect_tool(PRICE_CAPABILITY_ID)

)

print(price_schema)Inspect also gives you the information needed for routing. If one capability is unavailable for a region or asset class, the agent can choose another inspected candidate. Keep a cached copy of stable schemas, but refresh them periodically so provider changes do not silently break the monitor.

4Build the monitoring loop and anomaly detector

Call the selected capability with validated arguments, normalize the response into an internal observation, and compare it with a baseline. The example uses a percentage-change threshold for clarity; production systems should add volatility, time-of-day, liquidity, and data-quality checks.

from dataclasses import dataclass

from datetime import datetime, timezone

@dataclass

class Observation:

symbol: str

price: float

change_pct: float

volume: float

observed_at: str

async def fetch_quote(symbol: str) -> Observation:

result = await client.call(

capability_id=PRICE_CAPABILITY_ID,

arguments={"symbol": symbol},

)

data = result["data"] # Map fields from the inspected schema.

return Observation(

symbol=symbol,

price=float(data["price"]),

change_pct=float(data["change_pct"]),

volume=float(data.get("volume", 0)),

observed_at=data.get(

"timestamp",

datetime.now(timezone.utc).isoformat(),

),

)

def is_anomalous(obs: Observation) -> bool:

return abs(obs.change_pct) >= 2.0

async def scan_watchlist():

observations = await asyncio.gather(

*(fetch_quote(symbol) for symbol in WATCHLIST),

return_exceptions=True,

)

return [

obs for obs in observations

if isinstance(obs, Observation) and is_anomalous(obs)

]Add exponential backoff, provider-aware rate controls, timeouts, and stale-data checks before production. Store the raw response alongside the normalized observation so an analyst can audit the alert. Deduplicate events with a key such as symbol, trigger type, and time bucket; otherwise a persistent condition will create a new alert on every poll.

5Use Claude to generate a grounded alert report

Send only anomalous observations and relevant supporting evidence to the model. The model should summarize context, not invent missing market data or decide whether a trade must occur. Request JSON so downstream notification and audit systems can validate the response.

import json

from anthropic import Anthropic

anthropic = Anthropic(

api_key=os.environ["ANTHROPIC_API_KEY"]

)

def create_alert_report(observation: Observation) -> dict:

prompt = {

"task": "Explain this market anomaly for an analyst.",

"rules": [

"Use only the supplied evidence.",

"State uncertainty explicitly.",

"Do not provide a buy or sell recommendation.",

],

"observation": observation.__dict__,

"required_output": {

"headline": "string",

"why_it_triggered": "string",

"possible_context": ["string"],

"next_checks": ["string"],

"confidence": "low | medium | high",

},

}

message = anthropic.messages.create(

model=os.environ["ANTHROPIC_MODEL"],

max_tokens=700,

messages=[{

"role": "user",

"content": json.dumps(prompt),

}],

)

return json.loads(message.content[0].text)Model names and SDK behavior change, so confirm the current options in the Anthropic documentation. For higher assurance, validate the JSON against a schema and attach the original observation, source URL, capability ID, and execution ID to every report.

6Configure notifications and scheduling

Deliver alerts to the place where the team already works. The example posts a compact message to a Slack-compatible webhook. Email, Microsoft Teams, PagerDuty, or an internal event bus follow the same pattern. Keep notification delivery outside the detector so a temporary webhook failure does not block market-data collection.

import requests

def send_slack_alert(report: dict) -> None:

webhook = os.environ["SLACK_WEBHOOK_URL"]

body = {

"text": (

f"*{report['headline']}*\n"

f"{report['why_it_triggered']}\n"

f"Confidence: {report['confidence']}"

)

}

response = requests.post(webhook, json=body, timeout=10)

response.raise_for_status()

async def run_once():

anomalies = await scan_watchlist()

for observation in anomalies:

report = create_alert_report(observation)

send_slack_alert(report)

if __name__ == "__main__":

asyncio.run(run_once())Run this job with a scheduler such as cron, a managed cloud scheduler, or a durable workflow system. For sub-minute monitoring, prefer streaming or event-driven feeds over aggressive polling. Record heartbeat metrics so the absence of alerts is distinguishable from a stopped process.

Real-World Uses for Automated Market Monitoring

A fund can calculate volatility-aware thresholds across a 500-stock universe, enrich only the strongest anomalies with news and event context, and route alerts by sector or portfolio ownership. Analysts receive fewer but better-supported events.

A quant workflow can monitor momentum, liquidity, dispersion, correlation, or alternative-data factors in real time. The agent flags regime changes and packages the relevant observations for researchers without allowing an LLM to replace deterministic factor calculations.

The system can combine large wallet transfers, exchange inflows, funding rates, open interest, and spot-price movement. Cross-signal confirmation helps reduce alerts caused by a single transfer between known internal wallets.

A monitoring agent can connect a credible headline to the affected security, compare pre- and post-publication price behavior, and alert when both sentiment and market response exceed defined thresholds. News remains evidence, not automatic proof of causation.

Market events can be joined with internal positions, concentration limits, and scenario sensitivities. A risk alert then explains not only what moved, but why the move matters to the current portfolio and which exposure requires review.

Advanced Features for an AI Agent Financial Analysis Workflow

Once the basic loop is reliable, extend it carefully. Run multiple assets concurrently with bounded semaphores so parallelism does not overwhelm a provider. Store alert thresholds by asset, session, and strategy rather than using one global value. Backtest each trigger against historical data to estimate frequency, precision, and average time to meaningful follow-through.

Add suppression windows and event fingerprints to remove duplicates. Use a two-stage severity model: deterministic rules assign an initial priority, then the AI layer adds context without lowering a hard risk threshold. Integrate Slack or email only after building a durable alert store, because chat messages are difficult to audit. Finally, measure data freshness, capability latency, failed calls, model parsing errors, alerts per day, analyst dismissals, and confirmed useful alerts. Those metrics reveal whether the system creates intelligence or merely more notifications.

For authoritative reference data, developers may also compare provider documentation from services such as Alpha Vantage, Polygon, and official macroeconomic sources. QVeris reduces integration work, but source suitability, licenses, exchange entitlements, and latency requirements remain application decisions.

Production Checklist for a Market Monitoring AI Agent

Before enabling automated market monitoring for a real team, test the entire path rather than only the data call. First, verify clock synchronization and timestamp semantics. A quote timestamp, provider receipt time, agent processing time, and notification time represent different moments; mixing them can make a delayed observation appear current. Reject data older than the maximum age allowed by the strategy and make the age visible in every alert.

Second, design for partial failure. The monitor should continue scanning unaffected symbols when one capability times out. Use bounded retries, circuit breakers, and a fallback only when the fallback meets the same licensing and freshness requirements. Record which provider produced each observation so analysts can compare conflicting values. A silent switch from real-time to delayed data is worse than a visible temporary gap.

Third, separate detection from action. An alert may launch additional research, but it should not automatically create an order unless the organization has implemented independent controls, pre-trade checks, position limits, and explicit authorization. Give each alert a stable ID and lifecycle state such as new, acknowledged, investigating, resolved, or false positive. This turns notifications into an operational workflow instead of a stream of disposable messages.

Finally, test with replayed historical events and controlled failure drills. Simulate stale prices, malformed JSON, rate limits, duplicate news, missing volume, and an unavailable notification endpoint. Set service-level objectives for scan completion, data freshness, and delivery latency. An agent is ready for production when the team can explain what happened during both a valid alert and a failed monitoring cycle.

Conclusion: Launch Your AI Market Monitoring Agent

A production AI market monitoring agent combines reliable tool access, deterministic anomaly detection, contextual AI analysis, traceable evidence, and a notification policy that respects human attention. QVeris supplies a unified Discover → Inspect → Call layer for financial capabilities, while your application retains control over strategy, thresholds, permissions, and risk decisions. Start with one asset class and one measurable alert, validate it against historical behavior, then expand the signal set only when each addition improves decision quality.

AI 市场监控 Agent 解决的是一个看似简单但代价高昂的问题:金融市场产生的信息量远超人工团队持续监看的能力。报价以毫秒级更新,成交量结构不断变化,宏观数据按日程发布,一条新闻可能在分析师打开仪表盘之前就完成资产重新定价。错过信号会造成损失,但对每一次噪声波动做出反应同样危险。设计合理的 Agent 可以全天候收集证据,先用确定性规则识别异常,仅在需要时让 AI 模型解释背景,并发送带有可追溯来源的简洁预警。本指南将使用 QVeris 作为能力层、Python 作为编排层,完整展示这一流程。

什么是 AI 市场监控 Agent?

AI 市场监控 Agent 是一种能够自动观察市场数据、识别值得调查的情况并触发结构化响应的软件。响应可以是预警、投资组合风险检查、研究任务或人工审核请求。它与传统仪表盘不同,不需要人员一直盯着每个面板;它也不同于单一指标脚本,因为它能组合异构证据并解释事件为何重要。

实用的市场监控 AI Agent 可以监控实时价格和成交量,将当前行为与历史基线比较,追踪金融新闻情绪变化,观察来自 Federal Reserve Economic Data 等来源的宏观数据,并监控加密资产转账或流动性状态。最终报告应包含触发原因、关键数值、来源时间戳、置信度和下一步检查建议。

开发者选择自行构建,通常是因为监控逻辑与策略高度相关。通用产品可以支持固定观察列表和阈值,但量化团队可能需要因子感知的基线,金融科技产品可能需要租户级权限,风控团队则需要接入内部持仓。掌握编排层还能提高可解释性:每个阈值、工具调用和模型输出都可以记录和测试。

市场监控 AI Agent 应关注的核心信号

自动化市场监控的质量不取决于接入多少数据源,而取决于每类信号是否有清晰目的。建议先从五类信号开始,并在编写轮询逻辑之前定义什么才算真正有意义的变化。

阈值需要根据资产和交易时段调整。2% 的波动对大型股票可能异常,对小型代币却很常见。在调用 LLM 解释事件前,应先采用滚动分布、中位数绝对偏差或波动率标准化收益进行检测。确定性检测能控制成本并减少误报,模型只负责在系统确认异常后补充上下文。

为什么 QVeris 适合作为实时市场监控 AI 的基础

市场监控通常需要报价、K 线、公司事件、新闻、情绪、宏观数据,有时还包括链上活动。直接对接也可以实现,但每个供应商都有不同的认证方式、数据结构、速率限制、重试策略和故障模式。QVeris 将 10,000+ 金融能力统一在一个能力层中,让应用根据当前任务发现并执行合适工具。

整个流程分为三个职责。Discover 使用自然语言搜索能力,例如“带交易所时间戳的美股实时报价”;Inspect 返回所选工具的参数、输出结构、供应商信息、延迟和费用;Call 使用经过验证的参数执行能力并返回结构化结果。这样可以避免把所有工具都塞进 Agent 上下文,也不必将应用写死在单一供应商上。

QVeris 支持 REST、Python SDK,以及 Claude 和 Cursor 等 MCP 客户端。Discover 和 Inspect 永久免费,Call 会根据所选能力消耗积分。新账户目前赠送 1000 积分,并可通过每日登录获得 100 积分;请在 QVeris 定价页面确认最新规则。当 Agent 需要组合多个金融数据来源,同时又不希望维护大量自定义适配器时,这种架构价值最明显。

分步构建市场监控 Agent

下面的 Python 示例展示完整控制流程,同时保留供应商参数的灵活性。QVeris 能力 ID 和参数可能随工具更新而变化,因此请始终以最新 QVeris 文档和 Inspect 返回结果为准。API Key 应保存在环境变量中,并且模型生成的参数必须经过 schema 验证。

1注册并初始化 QVeris 客户端

注册 QVeris、生成 API Key,并将其保存在密钥管理器或本地环境变量中。按照官方文档安装当前 Python SDK。下面的客户端将作为发现、检视和调用能力的统一入口。

import os

import asyncio

from qveris import QVerisClient

client = QVerisClient(

api_key=os.environ["QVERIS_API_KEY"]

)

WATCHLIST = ["AAPL", "MSFT", "NVDA", "SPY"]认证信息与策略配置应分离。观察列表、轮询间隔和风险阈值可以进入版本控制,密钥则不能。生产环境还应定期轮换密钥,并从日志中移除授权请求头。

2发现实时价格与市场情绪能力

应根据期望的输出搜索,而不是直接指定供应商。一个查询寻找带交易所时间戳和成交量的实时报价,另一个查询寻找带来源信息的近期市场情绪。保存返回的能力 ID,随后先 Inspect 再执行。

async def discover_monitoring_tools():

price_tools = await client.discover(

query=(

"real-time US stock price, percentage change, "

"volume, exchange timestamp, structured JSON"

),

limit=5,

)

sentiment_tools = await client.discover(

query=(

"recent financial news sentiment for a stock ticker "

"with article source, timestamp, and sentiment score"

),

limit=5,

)

return price_tools, sentiment_tools

price_results, sentiment_results = asyncio.run(

discover_monitoring_tools()

)不要自动执行第一条结果。应按覆盖范围、延迟、可靠性、输出结构和成本对候选项排序。如果实时性是硬性要求,工作流需要拒绝延迟数据;如果用于研究,则可能接受延迟但历史信息更完整的来源。

3检视所选工具的 Schema

Inspect 会告诉应用,该工具需要股票代码、交易所、时间范围、周期、地区还是其他标识符。把必填字段转换成本地验证模型,缺少或不支持的值必须阻止执行。

async def inspect_tool(capability_id: str):

details = await client.inspect(

capability_ids=[capability_id]

)

return details

PRICE_CAPABILITY_ID = "CAPABILITY_ID_FROM_DISCOVERY"

price_schema = asyncio.run(

inspect_tool(PRICE_CAPABILITY_ID)

)

print(price_schema)Inspect 也为路由提供依据。如果某项能力不支持某个地区或资产类别,Agent 可以切换到另一个已经检视的候选项。稳定 Schema 可以缓存,但需要定期刷新,防止供应商变化导致监控静默失败。

4构建监控循环与异常检测器

使用经过验证的参数调用能力,把响应统一为内部 Observation,再与基线比较。示例为便于理解采用涨跌幅阈值;生产环境应增加波动率、交易时段、流动性和数据质量检查。

from dataclasses import dataclass

from datetime import datetime, timezone

@dataclass

class Observation:

symbol: str

price: float

change_pct: float

volume: float

observed_at: str

async def fetch_quote(symbol: str) -> Observation:

result = await client.call(

capability_id=PRICE_CAPABILITY_ID,

arguments={"symbol": symbol},

)

data = result["data"] # 按 Inspect 返回的 schema 映射字段。

return Observation(

symbol=symbol,

price=float(data["price"]),

change_pct=float(data["change_pct"]),

volume=float(data.get("volume", 0)),

observed_at=data.get(

"timestamp",

datetime.now(timezone.utc).isoformat(),

),

)

def is_anomalous(obs: Observation) -> bool:

return abs(obs.change_pct) >= 2.0

async def scan_watchlist():

observations = await asyncio.gather(

*(fetch_quote(symbol) for symbol in WATCHLIST),

return_exceptions=True,

)

return [

obs for obs in observations

if isinstance(obs, Observation) and is_anomalous(obs)

]生产环境还需要指数退避、供应商限速、超时和陈旧数据检查。原始响应应与标准化 Observation 一起保存,方便审核。可以用“股票代码 + 触发类型 + 时间窗口”生成去重键,否则持续异常会在每轮轮询中重复预警。

5接入 Claude 生成有依据的预警报告

只向模型发送异常 Observation 和必要的辅助证据。模型负责总结背景,不应编造缺失数据,也不应直接决定是否交易。要求模型输出 JSON,便于通知系统和审计系统进行验证。

import json

from anthropic import Anthropic

anthropic = Anthropic(

api_key=os.environ["ANTHROPIC_API_KEY"]

)

def create_alert_report(observation: Observation) -> dict:

prompt = {

"task": "Explain this market anomaly for an analyst.",

"rules": [

"Use only the supplied evidence.",

"State uncertainty explicitly.",

"Do not provide a buy or sell recommendation.",

],

"observation": observation.__dict__,

"required_output": {

"headline": "string",

"why_it_triggered": "string",

"possible_context": ["string"],

"next_checks": ["string"],

"confidence": "low | medium | high",

},

}

message = anthropic.messages.create(

model=os.environ["ANTHROPIC_MODEL"],

max_tokens=700,

messages=[{

"role": "user",

"content": json.dumps(prompt),

}],

)

return json.loads(message.content[0].text)模型名称和 SDK 行为会更新,请在 Anthropic 官方文档核对当前选项。更严格的系统应使用 JSON Schema 验证输出,并在每份报告中附上原始 Observation、来源 URL、能力 ID 和执行 ID。

6配置通知与定时任务

把预警发送到团队日常使用的平台。示例使用 Slack 兼容 Webhook,邮件、Teams、PagerDuty 或内部事件总线也可以采用同样模式。通知模块应与检测器分离,避免临时 Webhook 故障阻塞市场数据采集。

import requests

def send_slack_alert(report: dict) -> None:

webhook = os.environ["SLACK_WEBHOOK_URL"]

body = {

"text": (

f"*{report['headline']}*\n"

f"{report['why_it_triggered']}\n"

f"Confidence: {report['confidence']}"

)

}

response = requests.post(webhook, json=body, timeout=10)

response.raise_for_status()

async def run_once():

anomalies = await scan_watchlist()

for observation in anomalies:

report = create_alert_report(observation)

send_slack_alert(report)

if __name__ == "__main__":

asyncio.run(run_once())可以用 cron、云调度器或持久化工作流系统运行任务。对于亚分钟监控,应优先选择流式或事件驱动数据,而不是高频轮询。还应记录心跳指标,以区分“没有异常”和“进程已经停止”。

自动化市场监控的真实应用场景

基金可以在 500 只股票范围内计算波动率调整阈值,只为最强异常补充新闻和事件背景,并按行业或持仓归属路由预警。分析师收到的事件更少,但证据更完整。

量化流程可以实时监控动量、流动性、离散度、相关性或另类数据因子。Agent 负责标记状态变化并整理证据,但不能让 LLM 替代确定性的因子计算。

系统可以组合大额钱包转账、交易所流入、资金费率、未平仓量和现货价格。多信号确认有助于过滤交易所内部钱包之间的普通转账。

Agent 可以将可信新闻与相关证券关联,对比新闻发布前后的价格变化,并在情绪与市场反应同时超过阈值时预警。新闻是证据,但不能自动证明因果关系。

市场事件可以与内部持仓、集中度限制和情景敏感度结合。这样预警不仅说明什么发生了变化,也能解释为什么它会影响当前投资组合。

金融分析 AI Agent 可以增加的高级功能

基础循环稳定后,可以逐步扩展。使用有限并发同时监控多资产,避免并行任务压垮数据供应商。阈值应按资产、交易时段和策略分别保存,而不是使用一个全局值。通过历史数据回测每个触发器,评估出现频率、准确度以及发生后继续有效的平均时间。

加入抑制窗口和事件指纹以去除重复预警。可以使用两阶段严重性模型:确定性规则先确定初始优先级,AI 层只补充背景,不能降低硬性风险阈值。在接入 Slack 或邮件之前,应先建设持久化预警存储,因为聊天消息很难审计。最终需要监控数据新鲜度、能力延迟、调用失败、模型解析错误、每日预警量、分析师忽略率和确认有效的预警数量。

开发者还可以参考 Alpha Vantage、Polygon 以及官方宏观数据来源。QVeris 可以降低集成成本,但数据授权、交易所权限、来源适用性和延迟要求仍然需要由应用团队判断。

市场监控 AI Agent 的生产环境检查清单

在为真实团队启用自动化市场监控之前,需要测试完整链路,而不只是确认数据能够返回。首先检查时钟同步和时间戳语义。行情时间、供应商接收时间、Agent 处理时间与通知时间代表不同阶段;混用这些时间可能让延迟数据看起来像实时数据。应拒绝超过策略最大允许时效的数据,并在每条预警中明确展示数据年龄。

其次,要为局部故障设计系统。某个能力超时时,监控器仍应继续扫描其他股票。使用有限重试、熔断器和满足同等授权及新鲜度要求的备用能力。每个 Observation 都要记录实际供应商,方便分析师比较冲突数值。从实时数据静默降级为延迟数据,通常比暂时显示数据缺口更加危险。

第三,将检测与行动分开。预警可以触发进一步研究,但除非组织已经实施独立控制、交易前检查、持仓限制和明确授权,否则不应自动创建订单。为每条预警设置稳定 ID 和生命周期状态,例如新建、已确认、调查中、已解决或误报。这样通知才能成为可管理的工作流,而不是一次性消息流。

最后,通过历史事件回放和受控故障演练进行测试。模拟陈旧价格、错误 JSON、速率限制、重复新闻、成交量缺失以及通知端点不可用。为扫描完成时间、数据新鲜度和通知延迟制定服务目标。当团队既能解释有效预警,也能解释一次失败的监控循环时,Agent 才真正具备上线条件。

总结:上线你的 AI 市场监控 Agent

生产级 AI 市场监控 Agent 需要结合可靠的工具访问、确定性异常检测、带上下文的 AI 分析、可追溯证据,以及尊重人工注意力的通知策略。QVeris 提供统一的 Discover → Inspect → Call 金融能力层,而策略、阈值、权限和风险决策仍由你的应用掌控。建议从一种资产和一个可量化的预警开始,先用历史数据验证,再根据实际决策质量扩展信号范围。